The Current Landscape

The BAD Loans Company are relatively successful. Having invested a number of years ago in technology they have based their operations on this infrastructure which although aging is still allowing them to operate.

Recent digital investment from their competitors and new entries into the market place means that they are seeing increased competition, the company still has a strong account book of customers, who provide feedback to what they would like to see. Some of this feedback is listened to, although most change initiatives come from ideas that senior managers have seen implemented in previous companies.

In order to keep ahead of what is happening, the Execs have 4 key values…

Our Business

Although we grew rapidly over the last 5 years, our organisation is built on supplying sub-prime customers with cheap loans so in order to achieve this we have had to minimise our costs.

This means that our IT infrastructure has lacked investment and we are constantly looking for ways to reduce the overheads associated with our internal processes.

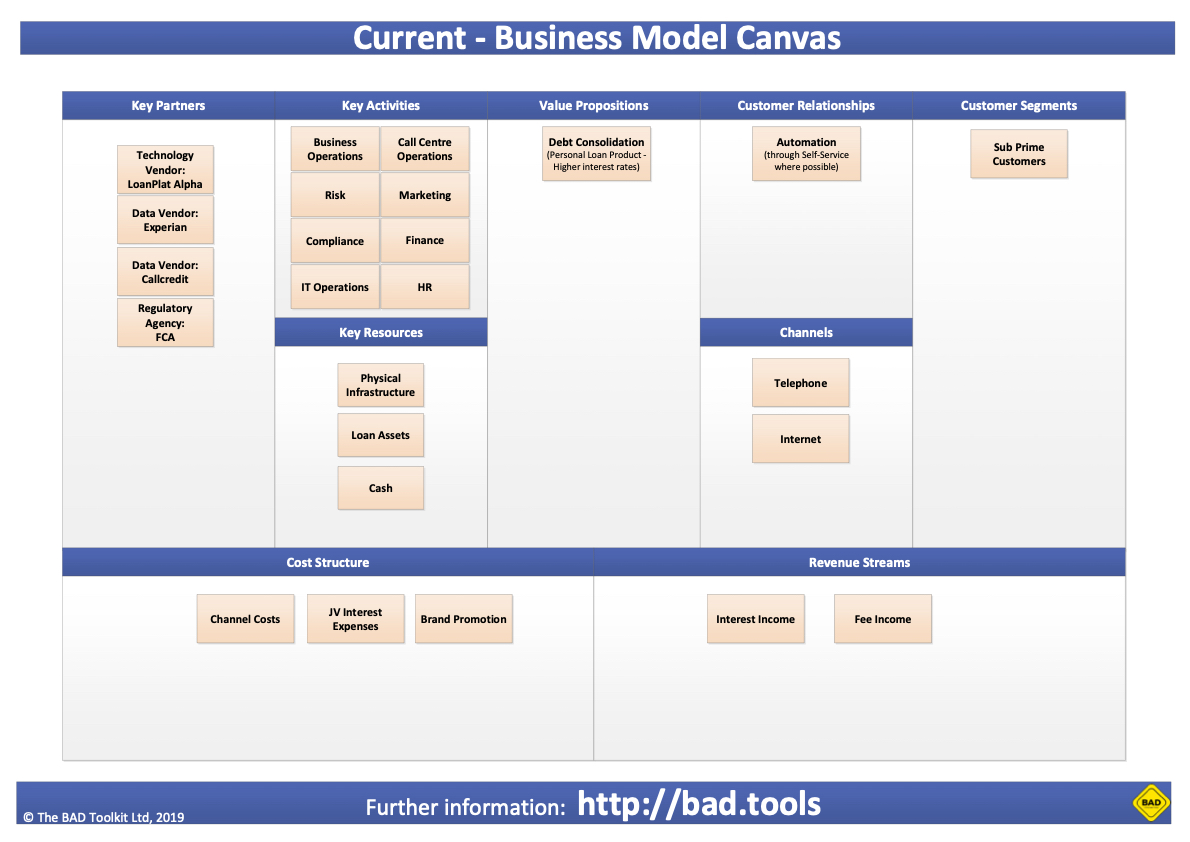

Our Data

At the BAD Loans company, we already invest in the use of data & insight to constantly monitor how we are performing. We do this by segmenting the data into Internal and External sources

Internally we monitor KPIs and harvest MI to feed into the exec teams. Over the last 12 months we’ve seen both operating costs and customer default rates go up, whilst our profit levels have continued to decline.

Externally the country is in the grip of both Brexit and the Global health crisis, both of which are expected to result in job losses and increase our default rates. In addition, our competitors are shifting from traditional high street stores to online which is further eroding our market share.

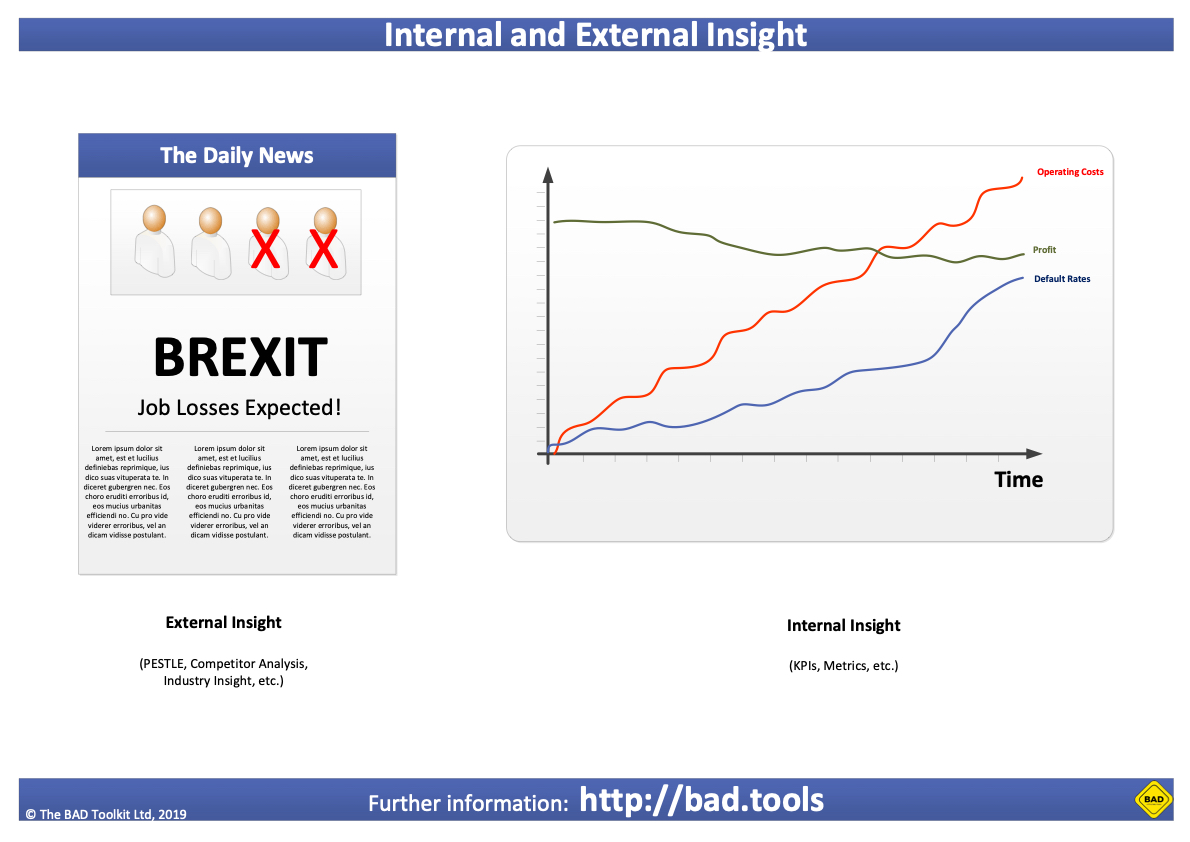

Our Customers

Our customers are jointly owned by marketing and customer services.

Our Customer Services Team find that customers are vocal in telling us what they would like to see and what is not working well for them. Sometimes this is direct feedback, however often is public via social media.

We also have some customer segmentation to show which customers are most valuable to us and marketing have previously worked with a external consultancy to identify what “typical” customers from each customer group would look like. This is only used to help with our brand marketing campaigns and is not utilised elsewhere in the organisation.